RBI maintains status quo; surprise with a downward revision of inflation

The Monetary Policy Committee (MPC) of the Reserve Bank of India(RBI), in its first bi-monthly policy meeting of fiscal 2018-19, kept the repo rate unchanged at 6 percent. While five out of six members supported the decision, one voted for a 25 bps hike. The decision was in line with the neutral stance of the policy with the objective to control inflation (marked by consumer price index (CPI)) at 4% within a band of +/- 2% and equally supporting growth. The decision of maintaining status quo was based on the uncertainty surrounded around the inflation trajectory due to 1) revision in minimum support price (MSP), 2) revision in house rent allowance (HRA), 3) fiscal slippages and monsoon.

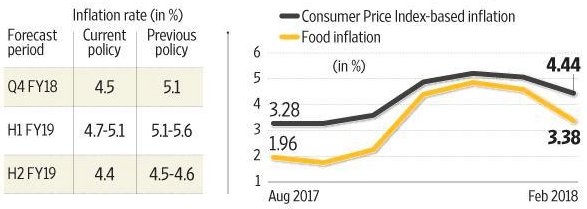

The decision of MPC was in line with the street expectation, however, the RBI left the participants with a surprise when it downward revised its inflation outlook for fiscal 2018. The downward revision in inflation was supported by recent moderation in food prices and statistically downside impact of pay revision related to seventh pay commission. The inflation forecast was revised as under:

Source: RBI, Centre for Monitoring Indian Economy and Livemint

We believe the status quo was expected and there could be no further change in rate on account of upside risk. Also, while inflation revision was expected but a reduction in the forecast for fiscal 2019 in its entirety was a surprise. Let us look at the upside risk:

The pressure around inflation building up; remains monitorable– Since the last MPC meeting in February 2018, the crude oil prices and metal commodity prices have been inching up. Also, if the announcement of 1.5x of the cost of production for MSP is implemented the food inflation could go high. Lastly, any deviation in the distribution of monsoon could impact on yield thereby the prices.

Lending rate tightening– Rising fiscal pressure resulted in an increased yield on the 10-year G-sec that increased from 7.2% in December 2017 to 7.6% in March 2018. Also, the banks started to increase lending rate due to expected non-availability of surplus in the banking system and the return of demand of bank borrowings from corporates.

We also believe that with subdued growth and tight liquidity, the RBI inflation risk seems to be overdone. However, there is no likelihood of rate revision until the monsoon spans out normally which could ease inflation to some extent. While there could be no revision for the next two quarters, we could see some prospects of revision towards the end of CY2018.

There has been a consistent improvement in the macroeconomic conditions as seen with the revival of manufacturing output, industrial production, healthy automobile sales and pick-up in credit. We believe the revised inflation from the RBI is a clear signal that developments are moving in the right direction and we could see growth propelling in. We believe accumulating good quality companies and adding up to current exposure with correction in valuation and price point could be a good investment strategy. We continue to remain bullish on the India strategy and believe the domestic theme currently playing is expected to stay and we would be able to see much-improved growth in earnings.

Created by Orowealth.com

No Comments